You can transfer the money from the UTMA or other custodial accounts to a 529 college savings plan. As custodian you will not be permitted to change the beneficiary of the custodial 529 plan..

Considering this, is a custodial account the same as a 529?

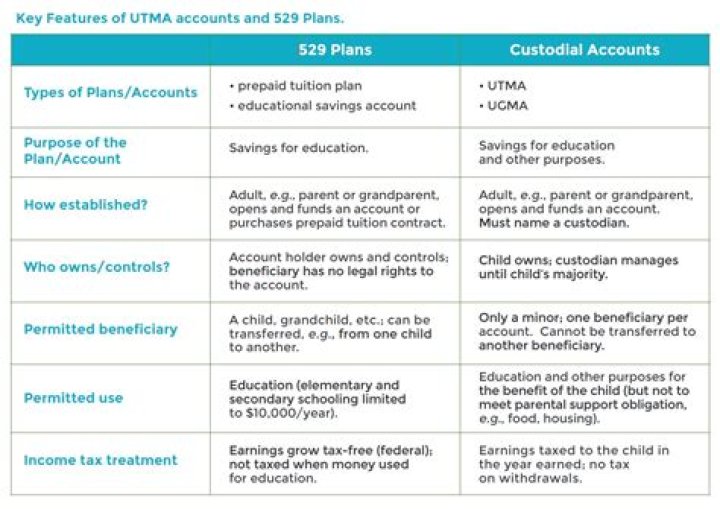

A 529 plan provides an investment vehicle designed for building funds to pay for college for children, while a custodial account acts as a trust that enables parents to store and invest assets for their children while the children remain minors.

Subsequently, question is, what is a custodial 529 plan? A custodial account is a savings accounts established for a child under the Uniform Gifts to Minors Act (UGMA) or the Uniform Transfers to Minors Act (UTMA). A custodial 529 plan account is a 529 plan owned by a minor child, who is also the named beneficiary on the account.

One may also ask, can I convert my custodial account to 529?

You can transfer the money from the UTMA or other custodial accounts to a 529 college savings plan. Since the money comes from an UTMA account, you must set up a custodial 529 college savings plan account, as opposed to a regular 529 plan account. The custodial 529 plan will be titled the same as the UTMA account.

Can you have two custodians on a 529 plan?

A 529 plan account has just one owner, which is fine when parents are together. However, when they split, each will have a separate stake in the child's education.

Related Question Answers

Do you pay taxes on custodial accounts?

While not tax-deferred, as are IRAs, custodial accounts do have some tax advantages. The IRS considers the minor child the owner of the account, so the earnings in it are taxed at the child's tax rate. Unearned income of more than $2,100 will be taxed at the parent's rate.How do you get money out of a custodial account?

Closing an Account You can close a custodial account and suffer no repercussions if you give the funds to the child or transfer them into another account for the child's benefit. You can close a custodial account and transfer funds to an education savings plan, for example, a 529 plan.Can a parent withdraw money from a UTMA account?

While a parent or custodian can withdraw UTMA/UGMA money at any time for the minor's benefit, the timing can be important as the minor approaches college age. In addition, some states prohibit parents from closing UTMA/UGMA accounts just before a child reaches that state's legal age of adulthood.Who is the owner of 529 plan?

A 529 plan must have an owner (such as a parent or grandparent) and a beneficiary (the student). The owner controls the contribution level, investment allocation and how and when to disburse funds. The owner also can change the 529 beneficiary.How does a custodial account work?

A custodial account is a financial account held in the name of a minor, usually by a parent, legal guardian, or another relative. If you are a parent or guardian of a young person, this gives you the opportunity to save and invest for your child while retaining full control of the account until they reach adulthood.What does custodial account mean?

A custodial account is a financial account (such as a bank account, a trust fund or a brokerage account) set up for the benefit of a beneficiary, and administered by a responsible person, known as a legal guardian or custodian, who has a fiduciary obligation to the beneficiary.Do custodial accounts affect financial aid?

For financial aid purposes, custodial accounts are considered assets of the student. This means that custodial bank and brokerage accounts have a high impact on financial aid eligibility. However, since 2009-10 the treatment of custodial 529 college savings plans has been more favorable.Is a custodial account a joint account?

Joint or Custodial Account A joint savings account lists both your minor child's name and your name as joint owners. This means that both you and your child have equal control of the account. A custodial account lists a minor child as the account owner, but with a parent or guardian as the account custodian.Which is better 529 or UTMA?

529 plans are also generally better for your taxes. Earnings in a 529 plan are tax-free as long as you use them for qualified education expenses. By contrast, the government taxes UTMA earnings above $2,100 like income from a trust or estate. This could mean a big tax bill.What happens to Utma when child turns 21?

Virtually all states have adopted some form of UTMA that allows you to make gifts to a minor to be held in the name of a custodian during the age of minority. On reaching the age of majority, usually 21 years, the minor is entitled to all assets held in the account.Can I roll an UTMA into a 529 plan?

You can move money from a custodial account, such as an UGMA (Uniform Gifts to Minors Act) or an UTMA (Uniform Transfers to Minors Act), to a 529 plan. But you can't do the reverse — transfer or convert from a 529 to a custodial account — without adverse tax consequences.Do I have to pay taxes on UTMA account?

UTMA accounts have a few tax implications. While there are no taxes on withdrawals (since contributions are made with after-tax dollars), there may be taxes on any unearned income. Unearned income includes taxable interest, dividends, and capital gains on any assets in the account.Do UTMA accounts have to be used for education?

While 529 plans provide for tax-free growth and distributions as long as the funds are used for educational purposes, there is no special benefit for spending money from a UTMA account on education. For most people, UTMA accounts are hassle-free until the child starts paying for college with funds from the account.How do I withdraw money from my UTMA account?

There are no IRS penalties on taking money out of a UGMA or UTMA account, but the investments purchased may have a surrender charge or exit fee if held less than a certain amount of time.Can Utma be transferred to another child?

Beneficiary Changes There is no ability to transfer a UGMA or UTMA account to another child or to change beneficiaries. At that point, the grown child is permitted to change the beneficiary from themselves to someone else, if he or she so desires.Can a minor own a 529 account?

Yes, you can. You're thinking of a custodial 529, or a 529 plan under the Uniform Gifts to Minors Act and the Uniform Transfers to Minors Act. It refers to account in a 529 plan funded with money already owned by your minor child. Nearly all 529 savings plans have special procedures to accommodate UGMA/UTMA 529s.How does a UTMA account work?

The Uniform Transfers to Minors Act (UTMA) allows a minor to receive gifts—such as money, patents, royalties, real estate, and fine art—without the aid of a guardian or trustee. A UTMA account allows the gift giver or an appointed custodian to manage the minor's account until the latter is of age.Does fafsa check bank accounts?

The FAFSA will specifically ask “As of today what is the cash balance of checking, savings…” accounts for the student. Because the question is phrased “As of today” it leaves room for interpretation. Cash assets sink financial aid eligibility, but are virtually untraceable unless admitted to on the FAFSA.Does having a 529 hurt scholarship?

Here's the high-level answer: 529s don't impact merit-based scholarships and they can minimize the impact of savings on need-based grants. Plus, if you get a scholarship, you can withdraw the amount of the scholarship without any penalty.