What did the repeal of Glass Steagall do?

.

In this way, why was the repeal of the Glass Steagall Act important?

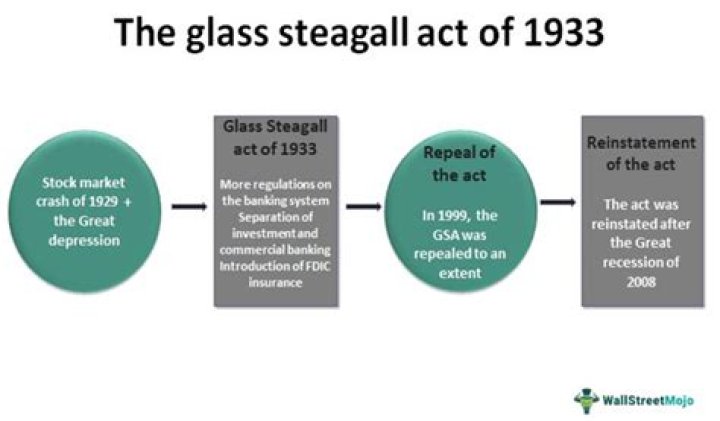

The Glass-Steagall Act of 1933 was enacted in response to the stock market crash of 1929. This bill was repealed in 1999 by the Gramm-Leach-Bliley Act because it was seen as being too restrictive for banks and businesses.

Similarly, who killed Glass Steagall? Gramm-Leach-Bliley Act One year later, President Bill Clinton signed the Financial Services Modernization Act, commonly known as Gramm-Leach-Bliley, which effectively neutralized Glass-Steagall by repealing key components of the act.

Consequently, is the Glass Steagall Act still around today?

In 2018, as part of a push to limit regulations, Dodd-Frank reforms were partially rolled back. Critics have sought to loosen Volcker Rule restrictions as well. Though the Glass-Steagall Act dates back to 1933 and has been partially repealed, it remains strikingly relevant today.

What is the repeal of the Glass Steagall Act by Congress in 1999?

Repeal of the Glass-Steagall Act Finally, after intense lobbying by industry groups, the Glass-Steagall Act was partially repealed in 1999 by the Graham-Leach-Bliley Act (GLBA)—specifically, its Section 20, which limited commercial banks' activities with their assets.

Related Question AnswersWhich President deregulated the banks?

In 1999 Congress passed the Gramm–Leach–Bliley Act, also known as the Financial Services Modernization Act of 1999, to repeal them. Eight days later, President Bill Clinton signed it into law.Did repeal of Glass Steagall caused financial crisis?

Wolff and others have tied Glass–Steagall repeal to the late-2000s financial crisis. Weissman agrees with Stiglitz that the "most important effect" of Glass–Steagall "repeal" was to "change the culture of commercial banking to emulate Wall Street's high-risk speculative betting approach."Why do we need Glass Steagall?

Purpose. Glass-Steagall sought to permanently end bank runs and the dangerous bank practices that created them. Congress passed Glass-Steagall to reform a system that allowed the failure of 4,000 banks during the Great Depression. It had debated the bill during 1932.What caused the 2008 financial crash?

The financial crisis was primarily caused by deregulation in the financial industry. That permitted banks to engage in hedge fund trading with derivatives. When the values of the derivatives crumbled, banks stopped lending to each other. That created the financial crisis that led to the Great Recession.What are three reasons why the Glass Steagall Act became less and less effective?

Three reasons the Glass-Steagall Act became less and less effective include: (1) new financial institutions and instruments were invented to circumvent the Glass-Steagall Act, (2) regulations covered fewer financial instruments, and (3) as the collective memory of the reasons for the regulations faded, politicalIs the Banking Act of 1935 still in effect?

The Act of 1935 made the FDIC permanent, and included the following provisions: All accounts would be insured up to $5,000. At this time 98.5% of all deposits were under the $5,000 limit. This was a dramatic change from the initial guidelines under the 1933 act.What does the Gramm Leach Bliley Act do?

The Gramm-Leach-Bliley Act (GLB Act or GLBA) is also known as the Financial Modernization Act of 1999. It is a United States federal law that requires financial institutions to explain how they share and protect their customers' private information.What did the Glass Steagall Act accomplish?

The Glass-Steagall Act effectively separated commercial banking from investment banking and created the Federal Deposit Insurance Corporation, among other things. It was one of the most widely debated legislative initiatives before being signed into law by President Franklin D. Roosevelt in June 1933.Who is responsible for the 2008 financial crisis?

The US treasury secretary in 2008, Paulson was the Sir Anthony Eden of the financial crisis. He had all the necessary credentials a Republican president would consider necessary for the job – chief executive of Goldman Sachs with an MBA from Harvard.What companies got bailed out in 2008?

| Date | Financial Institution | Amount |

|---|---|---|

| 10/28/2008 | Bank of America Corp.1 | $15,000,000,000 |

| 10/28/2008 | JPMorgan Chase & Co. | $25,000,000,000 |

| 10/28/2008 | Citigroup Inc. | $25,000,000,000 |

| 10/28/2008 | Morgan Stanley | $10,000,000,000 |