What is functional currency in accounting

A functional currency is the main currency that a company conducts its business. As companies transact in many currencies but report their financial statements in one currency, the foreign currencies have to be translated into the functional currency.

What is meant by a functional currency?

A functional currency is the main currency that a company conducts its business. As companies transact in many currencies but report their financial statements in one currency, the foreign currencies have to be translated into the functional currency.

What determines the functional currency?

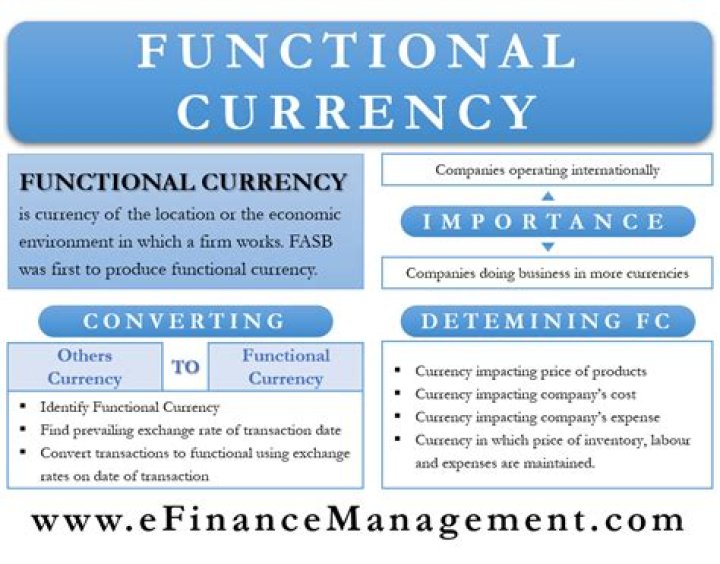

The functional currency is the currency in which an entity records and measures its transactions, in other words, the currency in which it maintains its accounting records. It is determined by reference to the currency of the primary economic environment in which that entity operates.

What is functional currency and examples?

The functional currency is the currency of the primary economic environment in which a company operates. … A company can decide to present its financial statements in a currency different from its functional currency, for example when preparing a consolidated report for its parent in a foreign country.What is the difference between functional currency and reporting currency?

The key difference between functional currency and reporting currency is that functional currency is the currency of the primary economic environment in which the entity operates whereas reporting currency is the currency in which financial statements are presented.

What is functional currency as per Ind AS?

Functional currency is the currency of the primary economic environment in which the entity operates. A group is a parent and all its subsidiaries. Monetary items are units of currency held and assets and liabilities to be received or paid in a fixed or determinable number of units of currency.

Can a company have 2 functional currencies?

A Only in rare circumstances will a branch have a different functional currency from its head office.

What are the two methods used to translate financial statements and how does the functional currency play a role in determining which method is used?

There are two main methods of currency translation accounting: the current method, for when the subsidiary and parent use the same functional currency; and the temporal method for when they do not. Translation risk arises for a company when the exchange rates fluctuate before financial statements have been reconciled.Does a group have a functional currency?

Conclusion. The notion of a group functional currency does not exist under IFRS; functional currency is purely an individual entity or business operation-based concept.

Can functional currency be changed?As described above, an entity’s functional currency reflects the underlying transactions, events and conditions that are relevant to it. Hence, once determined, the functional currency does not change unless there is a change in the underlying nature of the transactions and relevant conditions and events.

Article first time published onWhat does the term functional currency mean how is the functional currency determined under IFRS and under US GAAP?

IFRS Answer 028 IAs 21 says that the functional currency is the currency of the primary economic environment in which the entity operates. … Normally, it’s the currency in which the company makes and spends money. And, in most cases it will be just the currency of the country where you operate.

What is functional currency in SAP?

Functional currency is used for country or industry specific needs as an additional valuation currency besides local currency (the legal currency of the entity in its location) and group currency (the currency required by regulation or law in the group consolidation).

How do you change functional currency?

You simply need to translate all items of assets and liabilities into the new functional currency using the exchange rate at the date of change. For non-monetary items, this amount will be the item’s new historical cost. It means that you are NOT going to update the recalculation at the year-end with the closing rate.

What is functional currency for GAAP?

An entity’s functional currency is the currency of the primary economic environment in which the entity operates, normally the one in which it primarily generates and expends cash. Exchange differences on monetary items are recognised in profit or loss.

What is IND 105?

Ind AS 105 prescribes the accounting treatment for non-current assets held for sale and, and the presentation and disclosure of discontinued operations. It sets out the criteria for classification of a non-current asset (or disposal groups) as held for sale and discontinued operations.

What are the 27 accounting standards?

Accounting Standard (AS)Title of the ASRefer Note No.AS 25Interim Financial ReportingAS 26Intangible AssetsAS 27Financial Reporting of Interests in Joint Ventures7AS 28Impairment of Assets8

What is IND 113?

Indian Accounting Standard 113 (Ind AS 113) helps companies with a unified procedure to define the fair value of assets while declaring their financing statements. The standard, apart from setting a single framework for measuring fair value, also prescribes the methods of disclosures of fair value measurements.

What is functional currency under IFRS?

An entity’s functional currency is the currency of the primary economic environment in which the entity operates (ie the environment in which it primarily generates and expends cash). Any other currency is a foreign currency.

How does foreign currency affect financial statements?

Any and all adjustments between a foreign functional currency and the US $ are translation adjustments. Therefore the financial statements will be translated, not remeasured. This means that the affects of changing foreign currency exchange rates will be reflected on the balance sheet and not on the income statement.

What is temporal method?

The temporal method (also known as the historical method) converts the currency of a foreign subsidiary into the currency of the parent company. This technique of foreign currency translation is used when the local currency of the subsidiary is not the same as the currency of the parent company.

What are the four different methods used to translate financial statements from one currency to another?

There are four methods of measuring translation exposure: Current/Non-current, Monetary/Non-monetary, Current Rate, and Temporal methods.

What is the importance of functional currency?

It is important to establish the functional currency so that overall business performance can be properly measured and the financial statements can most accurately represent the true financial state of the company.

What is the difference between functional and local currency?

The local currency is the national currency of the country where an entity is located. The functional currency is the currency of the primary economic environment in which an entity operates.

How do you assess functional currency?

The functional currency is determined by looking at a number of relevant factors. This currency should be the currency in which an entity usually generates and spends cash. Functional currency should be the one in which the business transactions of an entity are normally denominated.

What FAS 52?

ASC 830 (aka FAS 52) provides the accounting and reporting requirements for foreign currency transactions and the translation of financial statements from a foreign currency to the reporting currency. …